News article topics: Receivership

Date: 21 August 2025

fixed charge appointment update")

The rising trend continues, with residential investments leading the way

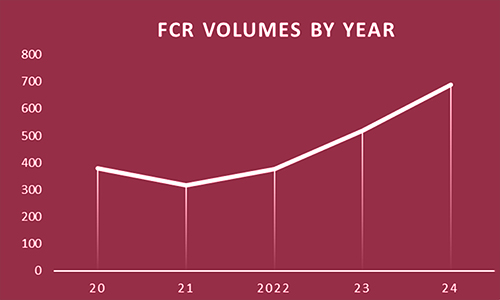

The inexorable rise in appointments for corporate borrowers continues. Reviewing the trend over the last four years sets the scene for the first two quarters of 2025.

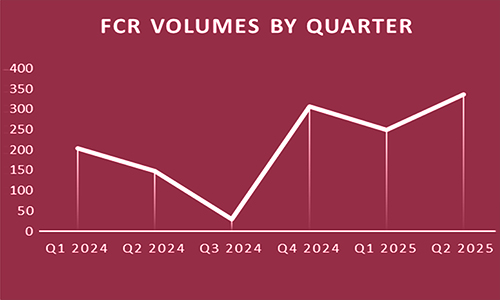

Due to delays in the registration of appointments, the quarterly figures for 2024 are distorted in showing a substantial reduction in Q3 (see below). This was resolved in Q4, with the overall trend showing clearly in the volumes by year.

Adding the figures for the first 6 months of 2025 continues that rising trend and shows an increase of 74% in Q1&2 ‘25 on Q3&4 ‘24.

Comparison of Q1&2 ’25 with Q1&2 ’24 shows a similar 67% increase.

Data for the month of July ‘25 – and which we felt might show a flood of appointments prior to the summer recess – shows in reality a reduced level. However, July 2025 is almost double that of July 2023 and three times that of July 2022. No meaningful comparison can be made with July 2024 due to the 2024 Q3 distortion.

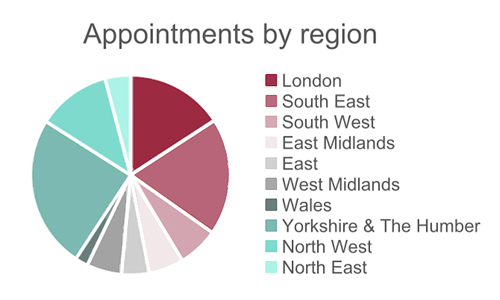

In terms of region, then for Q1&2 ’25 Yorkshire and the Humber surprisingly lead the pack at 25% (7% Q1&2 ’24), followed by the South East 19% (27%) and London at 16% (18%); the North West comes in at 12% (15%). Our view on Yorkshire (apart from its acknowledged charms) from the data we have, is the calling in of a large portfolio secured on a plethora of individual charges.

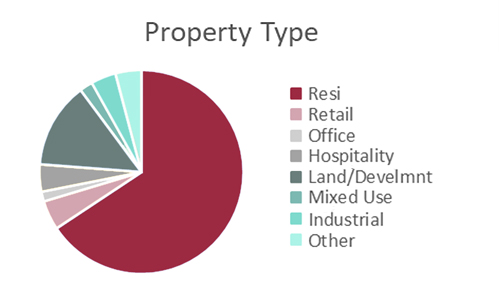

From the beginning of 2025 we undertook to provide a more detailed property type analysis. It is no surprise to see that residential is the overwhelming element at 65% of all appointments. Land and incomplete/part development ranks in second place at 14%; retail at 5%; hospitality at 4%.

We have concerns as to hospitality – we include hotel, guest houses, cafes, restaurants and bars – noting that this sector is appearing more and more within our figures. We believe this sector is likely to bear the brunt of current economic conditions most severely over the next few months.

As to the future, our members report a general unease in business activity within the SME sector, predicated on tighter margins resulting from increased material and labour costs, as well as uncertainty over the direction of the economy generally and the Exchequer in particular.

There is wide and varied speculation as to house price stability, although this varies materially from region to region, with increasing numbers of houses coming to the market.

It remains to be seen whether the recent reduction in interest rates – notwithstanding the latest inflation figures which continue to far exceed the BoE 2% target – will succeed in developing the economy: some have their doubts.

August 2025

Note: appointment refers to the individual charge – it may encompass a single unit, a development, or a portfolio; it is not a measure of individual properties.

Nara is the trade association for Fixed Charge Receivers. Founded in 1995 their professionally qualified members are trained in real estate insolvency, independently regulated and monitored. Recognised by both lenders and regulators, NARA is the pre-eminent voice of fixed charge receivership. Affiliate membership is free to lenders.

Contact: julian.healey@nara.org.uk

www.nara.org.uk