News article topics: Receivership

Date: 08 July 2026

Corporate Fixed Charge Appointments – Real EstateHalf yearly update - June 2026 |

|

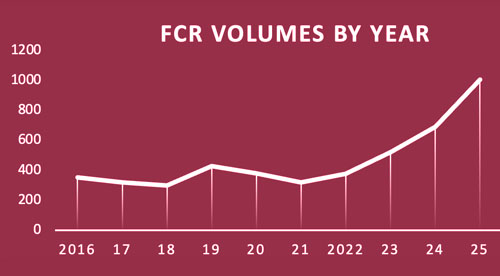

We continue to track corporate appointment levels by volume. economic region and sector. The first six-months of 2026 deliver no surprises in maintaining similar activity levels as Q1-2 in 2025. The last ten years nevertheless show an inexorable trend. It is too early to call whether that trend will continue for 2026.

So far in 2026 appointment (total) volumes1 have declined slightly when compared with the same half year period in 2025, but we are not yet back to 2024 levels 1 appointment refers to the individual charge – it may encompass a single unit, a development, or a portfolio: it is not a measure of individual properties.

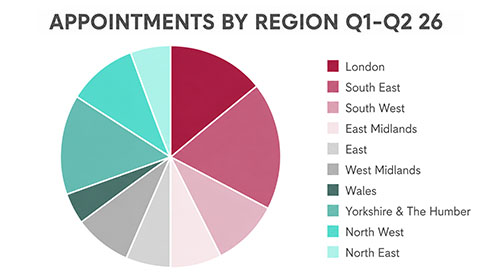

Volumes by economic region remain fundamentally unchanged

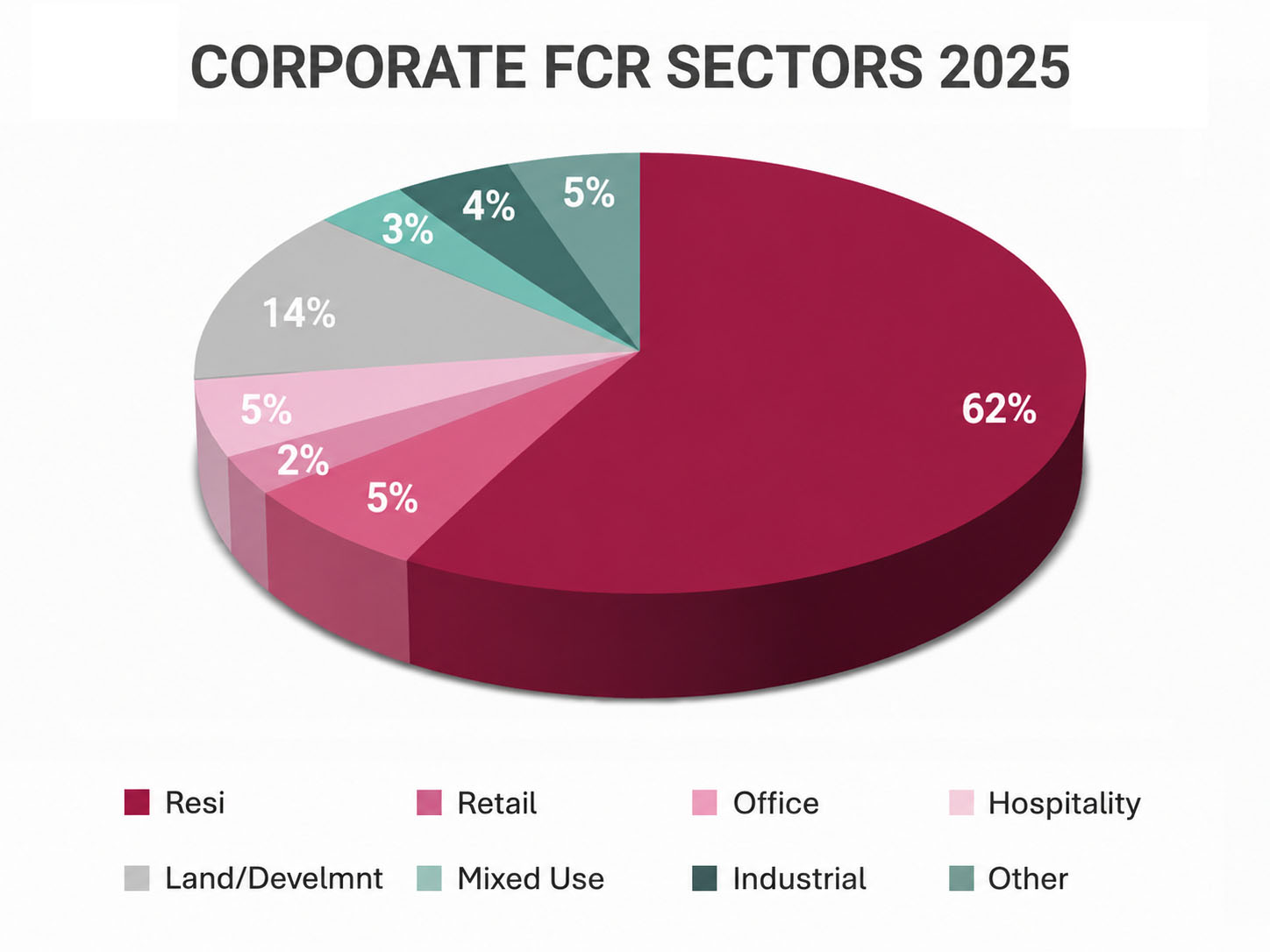

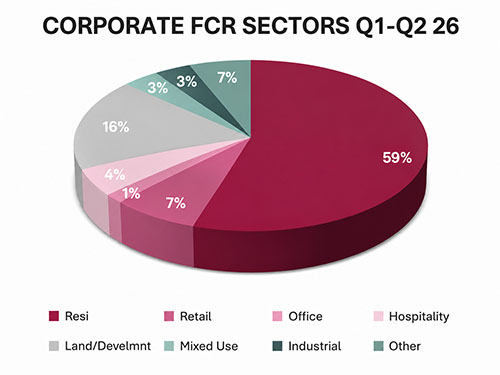

At face value, the same unchanged pattern applies to sectors when comparing 2025 in entirety to Q1-2 2026.

However, the consistently high residential figures bear further analysis. In 2026 we see a subtle shift in South East2 versus London3 figures. Throughout 2024 and 2025 the volume of South East residential appointments substantially exceeded London. The SE remains the greater, but the gap between the two is reducing, with increasing numbers of London residential appointments and reducing numbers for the SE. Hospitality remains at 5-6% but the figures show an increasing emergence of smaller care homes, while the 2025 surge of guest houses/private hotels apparently has now passed. Time will tell if that remains the case. Land and development similarly stay at 3-4% although we are seeing now both failed, completed projects as well as ever present part-built schemes, including some disastrous unfinished – dangerous, unprotected, scaffolded – remodelling/refurbishment projects. We cannot stress too strongly the need for the monitoring of such projects and early intervention to preserve latent value. The cost of reversing physical project deterioration increases exponentially with delay. Our statistics continue to show that clearing bank representation in appointment volumes, at this stage, remains steady at 3.5% (3.0% Q1-2 2025). 2 South East includes outer London

Nara membership sentiment bears witness to a nominal reduction in total appointments, but contrasts that with the notably increase in value of the appointments being made. Via AI, the threshold for borrower access to technical information is now much lower – no longer is there need for professional input. Inevitably, such complaints reflect the nature (almost always selective) of the facts inputted and the questions asked; additionally, AI regularly conflates differing legislation and even jurisdictions. |